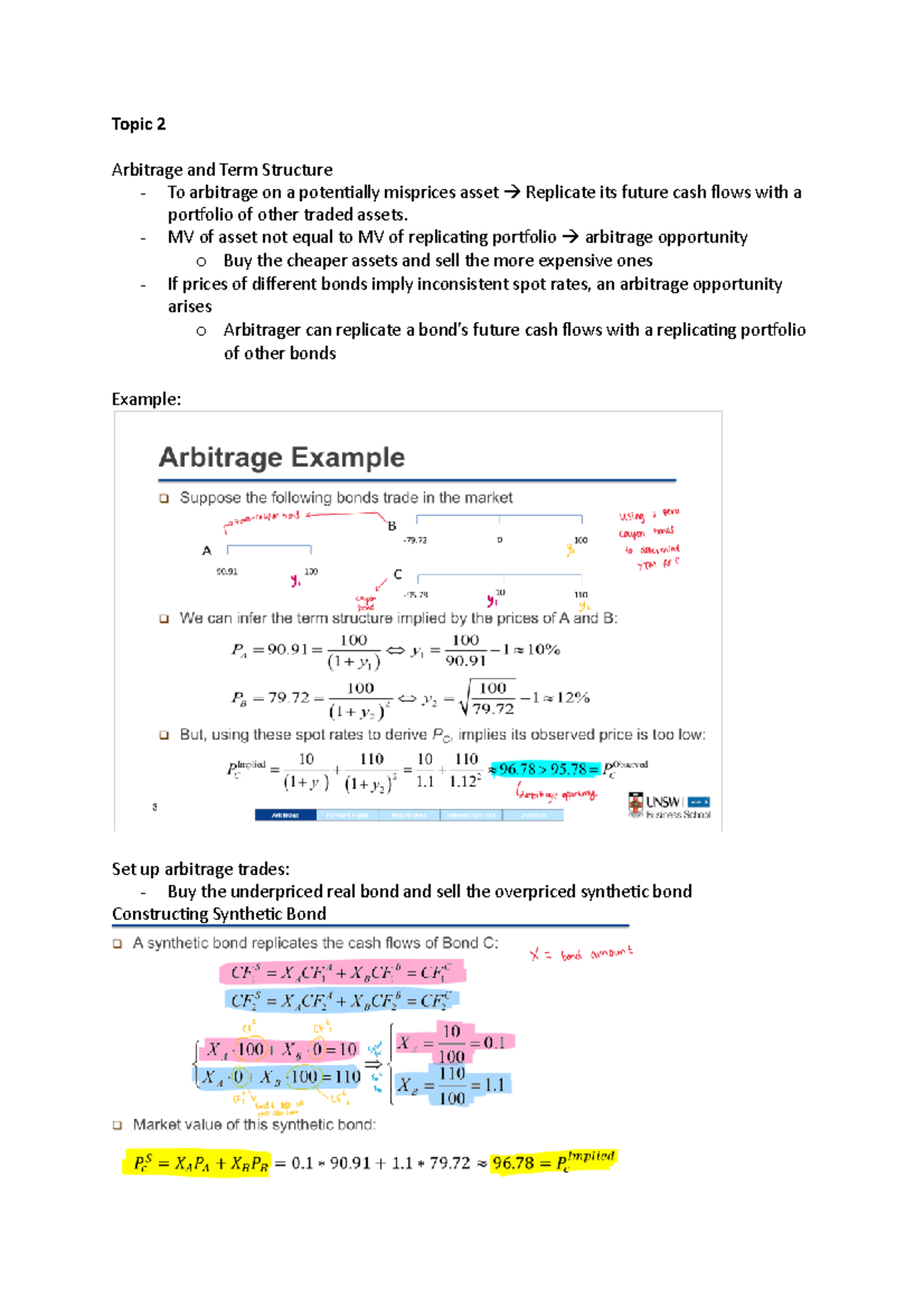

Financial advisors love to treat your life like a spreadsheet. They sit in climate-controlled offices, staring at actuarial tables, telling you that "patience is a virtue" and that claiming Social Security at 62 is a "permanent haircut" to your wealth.

They are wrong.

The conventional wisdom—the lazy consensus that you should wait until 67 or 70 to maximize your monthly check—is built on the flawed assumption that money today is worth the same as money tomorrow. It isn’t. It’s also built on the arrogant assumption that you will be healthy enough to enjoy that extra cash when you’re eighty.

Taking the money at 62 isn't "leaving money on the table." It’s taking your chips off the table before the house changes the rules.

The Breakeven Trap: A Mathematical Illusion

The "wait until 70" crowd relies on the breakeven analysis. They show you a chart where the cumulative total of your benefits finally crosses over at age 78 or 82.

Here is the problem: that analysis ignores the Time Value of Money. A dollar in your pocket at 62 is infinitely more valuable than a dollar promised to you at 80. Why? Because at 62, you can invest it, you can use it to pay off high-interest debt, or you can use it to fund a lifestyle while your body still functions.

If you take your benefits at 62 and invest them—even in a conservative portfolio—the "breakeven" point moves further and further into the future. If you achieve a 5% or 6% annual return, you might not "break even" until you are 90.

Are you willing to bet your life that you’ll be around at 90 to finally "win" the Social Security game? I've seen too many people spend their 60s "saving" for a 70s they never got to see. They died with a "maximized" benefit they never cashed. That isn't a strategy; it's a tragedy.

The Health Gradient: Your Knees Don't Care About COLA

Let’s talk about the biological reality that CFPs (Certified Financial Planners) ignore: The Go-Go, Slow-Go, and No-Go years.

- 62–72 (Go-Go): You can still hike, travel, and play with grandkids.

- 72–82 (Slow-Go): You’re slowing down. The bucket list is getting shorter.

- 82+ (No-Go): Your biggest expense is likely healthcare and rent in an assisted living facility.

The "experts" want you to starve your Go-Go years so you can be the richest person in the nursing home. It makes no sense. The utility of an extra $1,000 a month at age 63 is massive. It’s the difference between a trip to Italy and a trip to the grocery store. The utility of that same $1,000 at age 85 is marginal. It just pays for a slightly nicer brand of medication.

The Political Risk: The House Always Wins

The Social Security Trust Fund is projected to be depleted by the mid-2030s. Every "expert" will tell you, "Don't worry, Congress will fix it. They won't let it fail."

Maybe. But "fixing it" usually means one of three things:

- Raising the retirement age (again).

- Means-testing benefits (punishing you for having savings).

- Changing the Cost of Living Adjustment (COLA) formula to a "chained" CPI that grows slower.

When you claim at 62, you are "grandfathered" into the current system. You are a recipient. You are a voter with a check already in the mail. It is politically much harder to claw back money from someone already receiving it than it is to change the rules for someone "waiting" to join the club.

I’ve spent twenty years watching how policy is made. If you think the "rules of the game" won't change in the next decade, you aren't paying attention. Claiming early is a hedge against political volatility. It’s a bird in the hand.

The Tax Efficiency Maneuver

If you have a sizeable 401(k) or IRA, waiting until 70 to claim Social Security can actually create a "tax bomb."

When you hit age 73 (under current SECURE 2.0 rules), you are forced to take Required Minimum Distributions (RMDs). If you also waited until 70 to get that massive Social Security check, your taxable income spikes. This can push you into a higher tax bracket and trigger the IRMAA (Income-Related Monthly Adjustment Amount), which makes your Medicare premiums skyrocket.

By taking Social Security at 62, you provide a floor of income that might allow you to leave your IRA untouched, or better yet, perform Roth Conversions between ages 62 and 73 while your income is lower. This allows you to move money from a "forever taxed" bucket to a "never taxed" bucket.

The "wait until 70" advice is a one-size-fits-all solution for a world that is anything but.

Dismantling the "Expert" Questions

People often ask: "Won't I regret having a smaller check for the rest of my life?"

Only if you spent the money on depreciating garbage. If you used the early checks to bridge the gap so you didn't have to sell stocks during a market downturn (Sequence of Returns Risk), you won’t regret it. You’ll be grateful you had a cash cushion that didn't depend on the S&P 500.

Another common query: "What about my spouse?"

This is the only area where the contrarian view needs a reality check. If you are the high earner and your spouse has little to no earnings history, your "survivor benefit" is based on when you claim. If you die first, they get your check. If you claim at 62 and die at 70, you’ve locked your spouse into a lower lifetime benefit.

But even here, the logic holds: if your spouse is also in poor health or has their own robust pension, the "survivor benefit" argument loses its teeth.

The Opportunity Cost of Labor

Every year you "wait" for a higher check is often a year you feel pressured to keep working a job you might hate.

What is the price of your freedom? If claiming at 62 allows you to quit a soul-crushing corporate gig three years earlier, the "math" doesn't matter. You cannot buy back your 60s. You cannot go back and visit your parents or travel with your spouse when you’re both 75 and one of you has a hip replacement.

We have been conditioned to maximize wealth when we should be maximizing well-being.

The Brutal Truth

The financial industry hates the "Claim at 62" movement because it encourages people to stop working and start consuming. They want your assets under management (AUM) for as long as possible. They want you to keep contributing to your 401(k) and keep your hands off your "nest egg."

If you claim Social Security at 62, you might draw down your private investments more slowly. That’s less profit for them.

Stop looking at Social Security as an investment account that needs to "grow." It isn't. It is an insurance policy against longevity. But if you have other assets, you don't need to "maximize" the insurance; you need to "optimize" your life.

Take the money. Spend it on the things that matter while you still have the energy to do them. Stop being a slave to a spreadsheet that doesn't know your name or the state of your health.

Grab the check at 62 and run.